Note: This article is the fifteenth in an ongoing series on valuation and capitalization. To learn more about the financial mechanics of early stage investing, download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.

Have you ever been in a situation where you are negotiating an investment with an entrepreneur and you can’t agree on the pre-money valuation? Any early stage investor who makes more than one or two investments will certainly run into this issue. It’s never an easy discussion, so it helps if you are prepared ahead of time with concrete facts and figures for your recommended valuation. If you do a little homework, not only might you be surprised how little difference small changes in valuation make for founders, you will also be armed to have a very educational discussion with the entrepreneurs.

Have you ever been in a situation where you are negotiating an investment with an entrepreneur and you can’t agree on the pre-money valuation? Any early stage investor who makes more than one or two investments will certainly run into this issue. It’s never an easy discussion, so it helps if you are prepared ahead of time with concrete facts and figures for your recommended valuation. If you do a little homework, not only might you be surprised how little difference small changes in valuation make for founders, you will also be armed to have a very educational discussion with the entrepreneurs.

Let’s play out a scenario that Christopher and I ran into recently with a company in which we were looking to invest. At a high level, here are the key facts about the company today, along with a few assumptions we will make about the future of the company.

-

The company is pre-revenue and needs to raise $1.25M to get their product shipping and close their first few customer deals.

-

We were willing to invest at a $3.6M pre-money valuation. The entrepreneur insisted on a $4M valuation.

-

We assumed the company will need an additional $5M Series B financing to get all the way to an exit.

-

We assumed the Series B round will be priced at 2X the post-money valuation of the Series A round, and both rounds will be Non-Participating Preferred.

-

We assumed that approximately 5% of the common shares are held by employees, directors and advisors.

-

We assumed an exit for the company will be somewhere in the $25M to $100M range.

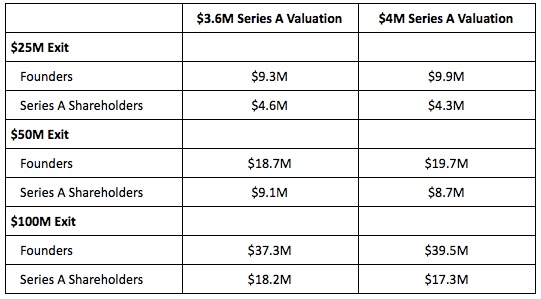

So, given those facts and assumptions, what difference does our requested valuation ($3.6M) versus the entrepreneur’s desired valuation ($4M) actually make to the returns of each party?

Note that our $3.6M pre-money offer is 10% less than the founder’s $4M pre-money expectation. The final outcome for the entrepreneur in all of the above exit scenarios shows about a 5% to 6% difference in what they will ultimately receive upon an exit. Even though it feels to the entrepreneur that our respective valuations are miles apart, the reality is about half the difference in the end.

It is probably worth pointing out to the entrepreneur that there are two further advantages for them in keeping the pre-money reasonable:

It makes it easier to bring investors into the round so that they can finish the fund-raising quickly and get back to focusing on the operations of the company. And, it means the post-money valuation will be more reasonable, which means it will be less of a yoke around their necks as they head into the uncertainties that lie ahead and try to grow into justifying their valuation for the next round.

So hopefully you are convinced it is worth doing some modeling. But how can you easily do this type of financial modeling to help better understand valuation and exit scenarios? You need a good Cap Table and Waterfall Analysis tool.

If you perform a Google search for the term “Cap Table”, you will end up with dozens of options to choose from. These options include everything from Excel spreadsheets that build simple cap tables all the way along the spectrum to complex, high-end software products that will track everything you need for a complete cap table. But we built ones we think you might prefer using.

Download the Series A Cap Table Spreadsheet >>

Download the Series A & B Cap Table Spreadsheet >>

So why did we bother creating another cap table tool when there are so many options out there? We did it for several reasons:

-

We wanted a tool that was very simple to set up. We didn’t want to have to enter lots of data to model a cap table.

-

We wanted a tool that allowed us to model a variety of different exit scenarios to help understand how much each shareholder would get depending on the size of the exit.

-

We wanted a tool that was free for everyone to use with no strings attached.

We chose the familiar Google Sheets platform and created two separate documents. The first sheet allows you to create a cap table with just a single Series A round of financing for very basic modeling. The second sheet allows you to create a cap table with both a Series A and Series B round. In both sheets, we provide a waterfall analysis so you can model exactly how much capital is returned to each shareholder and each class of stock under a variety of exit scenarios.

These sheets were designed with a fairly common capitalization structure in mind. The sheets support the following key features:

-

Either one or two rounds of Series Preferred Stock

-

Participating and Non-Participating Preferred Shares

-

Liquidation Preferences

-

Options, both Issued and Non-Issued

-

Waterfall Analysis to model multiple exit scenarios

It’s also important to note that for the sake of simplicity and usability these sheets are NOT designed to support the following items commonly found in cap tables:

-

More than two rounds of Series Preferred Stock

-

Convertible Notes

-

Dividends

-

Warrants

So, if you are looking for a complete solution that will help you manage every aspect of your company’s cap table, just do a Google search and you will find plenty of great products to purchase. In the meantime, try out these free Google sheets to help you build a well structured cap table along with a waterfall analysis for exit scenario modeling.

Download the Series A Cap Table Spreadsheet >>

Download the Series A & B Cap Table Spreadsheet >>

Next up in this series: Seraf Toolbox - Modeling Tool for an Early Stage Investment Portfolio.

Want to learn more about the financial mechanics of early stage investing? Download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.