Note: This article is the thirteenth in an ongoing series on valuation and capitalization. To learn more about the financial mechanics of early stage investing, download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.

How do you define success as an angel investor? Are you successful if you invested in one grand slam like Amazon or Google? Perhaps you define success as not losing all of your angel investment dollars after making investments in a dozen companies. Or, maybe success for you is defined by how many entrepreneurs you helped get companies financed and on their way. Since angel investors have many different criteria for defining success, it’s difficult to compare one investor’s results to another’s.

With all that said, I’d like to propose we narrow the focus temporarily and take a purely mathematical approach to defining success. This approach is similar to the method used to measure the performance of traditional VC funds. There’s a significant amount of data collected over the years for VC performance from organizations such as Cambridge Associates and Thomson Reuters Venture Economics. And, even though there is limited data on angel investing returns, we do have some preliminary research that indicates average returns for angel investors are around 27% for an annual rate of return.

If you are motivated by financial performance in angel investing, just as Ham and I are, what level of investment returns do you need to achieve before you declare success? Let’s ask Ham what financial yardstick he likes to measure his performance against and find out how he expects his investment returns to materialize over the years.

Ham, what data from the VC world do you think will help angel investors understand what performance metrics they should use as guidelines when measuring their own performance?

Let me start by briefly explaining how VC funds are structured. A typical fund has a fixed amount of capital (e.g. $250M) to invest. Most funds have a 10 year life span where most of the new investments are made in the first three years and follow-on investments are made in the subsequent years, with increasing focus on enabling exits as the fund reaches maturity. The expectation of the VCs is that most, if not all, of their investments will have an exit before the end of the 10 year fund life. Though, it should come as no surprise to know that many funds are extended by an additional 2-3 years before being shut down.

Because the risks investing in startup companies are much greater than the risks of investing in public companies, and the money is totally tied up and illiquid throughout, VC funds need to outperform the public stock market indices (S&P 500, NASDAQ 100, etc.) by a significant amount to make economic sense. So an annual 10% rate of return for an investor in a VC fund is not enough. They are looking for annual return percentages in the high teens or low twenties. And keep in mind that their performance threshold is raised by the fact that they are taking management fees out as they go along, and also taking a carry out of profits, which further reduces the take-home performance of their LPs.

Based on detailed research from Cambridge Associates, the top quartile of VC funds have an average annual return ranging from 15% to 27% over the past 10 years. So, if you are an investor in one of these top quartile funds, your returns are better than what you would expect to achieve in the public market indices. However, if you invested in one of the bottom quartile VC funds over the past 10 years, your returns are mostly in the low single digits. You would have been better off in a fund that tracks the S&P 500 (and you would have paid a lot less in fees)!

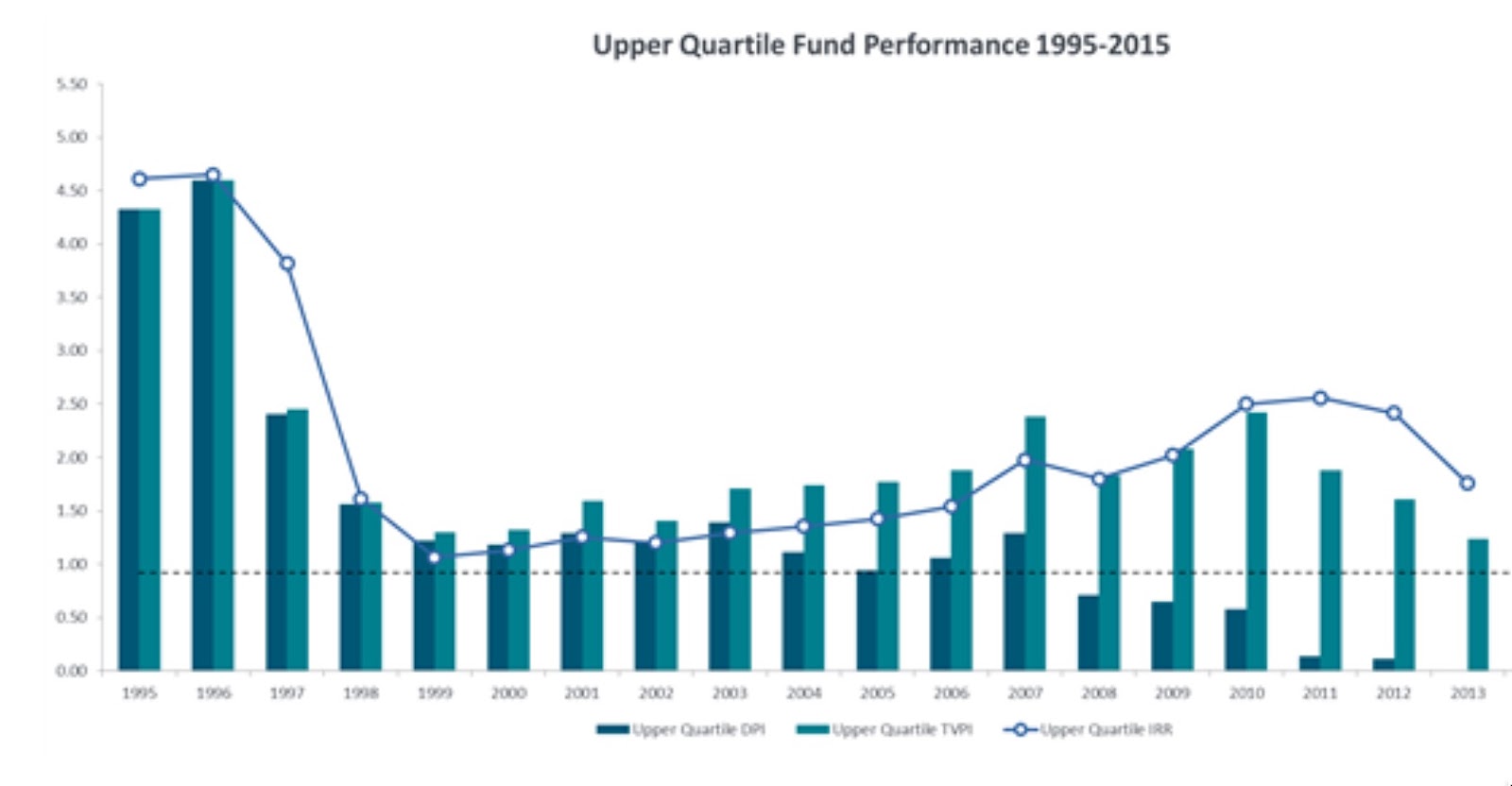

In addition to analyzing annual rates of return, it’s helpful with VC funds to look at the Distributed to Paid-In (DPI) ratio and the Total Value to Paid-In (TVPI) ratio. The DPI ratio is a calculation of the total amount of capital returned to the investors divided by the amount of capital invested into the fund. The TVPI ratio includes capital return to the investors along with any remaining value still in the fund. As you can see in the Cambridge Associates chart below, the TVPI ratio (light blue bars), goes as high as 4.5x in the boom years of the Internet bubble and down to 1.5x during the post bubble years. It should be noted, if you want to be a top decile fund, your final DPI ratio needs to be around 3x. In other words, for every 1 dollar invested in a VC fund, there needs to be a return of 3 dollars over the subsequent 10 year time period. Taken together these VC performance indices should give angels a sense of what the professional money managers achieve when working with these startup companies (albeit at a slightly later stage.)

The data from Cambridge Associates talks about the overall returns from venture funds. How should angel investors think about the returns they will get from an individual company in their portfolio?

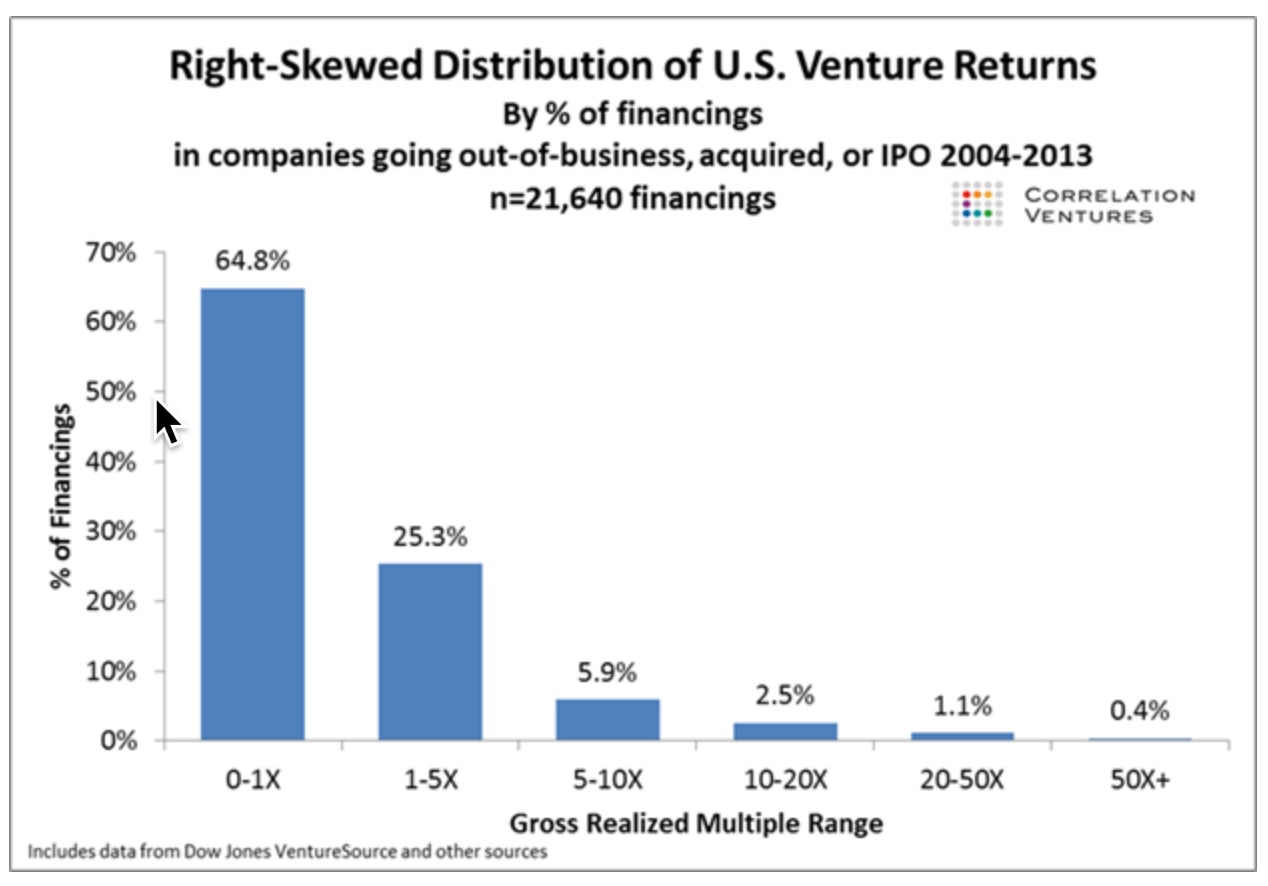

In a previous piece, we talk about what you should expect the exits to look like in a portfolio of 10 companies. In summary, we indicated that if you are using a good process and working out of a strong deal flow, you can expect to end up with approximately 5 strikeouts, 4 base hits and 1 home run in any batch of ten companies. For a more detailed analysis, Correlation Ventures researched more than 21,000 exits of VC-backed companies between 2004 and 2013.

Based on the data from Correlation Ventures, you can see in the chart above that approximately 65% of companies return 0 to 1 times the capital invested. Those are your strikeouts. Another 25% of companies return 1 to 5 times the capital invested. Those are your base hits. The remaining 10% return more than 5 times the capital invested. And, that’s where your home runs come from. If you are really lucky, over the course of a few 10 company “baskets” you have one of the 50x+ returns that qualify as a grand slam.

It’s important to note that these results are for VC-backed companies. Angel investors fund a wider range of companies, and in many cases, invest at earlier stages, with lower valuations and higher alpha, than VCs with correspondingly higher valuations at their initial time of investment. Based on the data that we have collected at Seraf over the years, we see a somewhat lower percentage of failures in our dataset and a slightly larger number of home runs versus what Correlation Ventures reports for the VC industry. Though, in fairness, the Seraf portfolio management platform may cater to the more organized, serious and professional half of the angel market.

Now we know what a great VC fund looks like (it should return 3x capital invested). And, we know what the return distribution should look like for early stage investments (a mix of strikeouts, base hits and home runs.) How do we combine that information to help an angel investor construct a great performing portfolio?

My job explaining how to build an angel portfolio would be so much easier if angels invested through a fund model similar to what VCs do. So, to help grasp the math behind structuring a successful fund, I am going to make the following simplified assumptions for this simplified example angel investor portfolio.

-

The angel will invest in 10 companies, which we believe is really the minimum needed for baseline diversification.

-

Most likely all of the initial investments will be made over a 2 to 3 year time period.

-

To keep it simple, each company will receive the same amount of investment. So for a small angel portfolio of $250K, each company will receive a $25K investment.

-

There won’t be any follow-on rounds of investment and the entire portfolio of companies will exit within 10 years of the first investment made by the angel.

Given those assumptions, how can this angel end up making 3 times her money in ten years? What does the math have to look like to achieve this level of success? Without the aid of smart follow-on investments, it is not easy. Using the expected distribution of exits that we see from the Correlation Ventures chart above, and applying our learnings on angel exits from Seraf, we come up with the following for a top quintile (3X DPI) angel portfolio.

-

5 companies in the portfolio are total losses and return $0 to the investor. However, you are able to get 20% of your investment back through an offset vs. any capital gains you have. This means each company will return $5K in tax writeoffs for a total of $25K.

-

You might not like the fact that I used tax benefits as part of the investment returns. So instead, consider that at least one or two of these failed companies will return some capital. That’s another way you can get $25K back from your initial $125K investment in these 5 companies and still consider the investments in the strikeout category.

-

3 of the remaining 5 companies average out to 3X on invested capital, so each company returns on average $75K for a total of $225K. Combined with the 25K from the losers you are now at a break-even $250K or 1X.

-

1 company produces a 5X return, not a bad exit, but nothing to set the world on fire. This company returns $125K.

-

1 company is the real winner in the portfolio (15X) and does the heavy lifting you need to achieve a high rate of return. Without this exit, it’s hard to justify the risk that an angel investor takes with their capital. This company returns $375K.

-

So the combined return on all 10 companies is $750K. That’s a 3X return on the angel investor’s original investment of $250K.

Many angel investors believe they have to invest in the next billion dollar company to achieve big returns on their angel investments. The reality, based on the assumptions outlined above, is that you don’t. In my personal portfolio, I’ve had two home run exits (i.e. 10-20X level). One company was acquired for less than $50M and the other for less than $200M. Find two companies like that in a 10 company portfolio and you are well on your way to awesome angel investment returns!

In the example outlined above, if the investor had more money for greater diversification or some follow-on investment in some of the winners, there would be a bit more room for error. But still, this simple angel portfolio example should help you understand how fund math works. For a more detailed approach to modeling a portfolio, we’ve put together a sample spreadsheet that will allow you to model a variety of scenarios. Check it out and see what other ways you can achieve a successful financial outcome for your angel investments.

Next up in this series: Pure Upside: Understanding Stock Options and Restricted Stock for Angels.

Want to learn more about the financial mechanics of early stage investing? Download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.