Note: This article is the seventh in an ongoing series on valuation and capitalization. To learn more about the financial mechanics of early stage investing, download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.

After considering exit practicalities for the company in Worksheet One of the Seraf Method, the purpose of Worksheet Two is to gauge how much capital it is going to take to move the company to the most logical point of exit and estimate the impact that financing plan should have on the valuation you should pay. This is important to assess in the valuation context because, as we have discussed previously, more capital required means more financing risk and more dilution for you, both of which drastically affect your returns. Capital should also enable more growth, but it definitely does mean more financing risk and dilution.

After considering exit practicalities for the company in Worksheet One of the Seraf Method, the purpose of Worksheet Two is to gauge how much capital it is going to take to move the company to the most logical point of exit and estimate the impact that financing plan should have on the valuation you should pay. This is important to assess in the valuation context because, as we have discussed previously, more capital required means more financing risk and more dilution for you, both of which drastically affect your returns. Capital should also enable more growth, but it definitely does mean more financing risk and dilution.

As we discussed in Approximations, Assumptions and Aspirations: Methods For Valuing Startups, even thriving companies require cash to grow. Let me repeat that for emphasis: growth consumes cash. The reason for that is fairly obvious if you think about it. Take buying a car, for example. Do you pay up front and then have someone go make a car for you? No, walk into a dealership, plunk your money down, and drive out in a car that was already sitting there on the lot. The car company had to design the car, build the factory, purchase the parts, pay the fabricators, and ship the car to the dealer before it could be sold to you. All those things required the seller to burn working capital long before they had your money to defray the costs. If the car company is to grow, it needs to invest working capital. If it is to grow fast, it needs to invest lots of working capital.

Startups are no different. They need to build a product and figure out how to sell it before they get paid for it. So some additional financing is virtually always required if the company is going to realize its fastest possible growth potential. The terms on which that money comes in will determine whether early investors do well and experience mere arithmetic dilution, or do poorly and experience the feared economic dilution.

The terms on which additional money comes in are driven by two things: (1) how well the company executes and (2) the nature of the company’s business model and go-to-market approach.

-

Execution: The team’s likelihood of executing well is an intangible due diligence question we have talked about at length elsewhere. We strongly believe that backing excellent teams is critical to success. So for the purposes of this model, we have to assume you are putting a valuation on a company with a solid team.

-

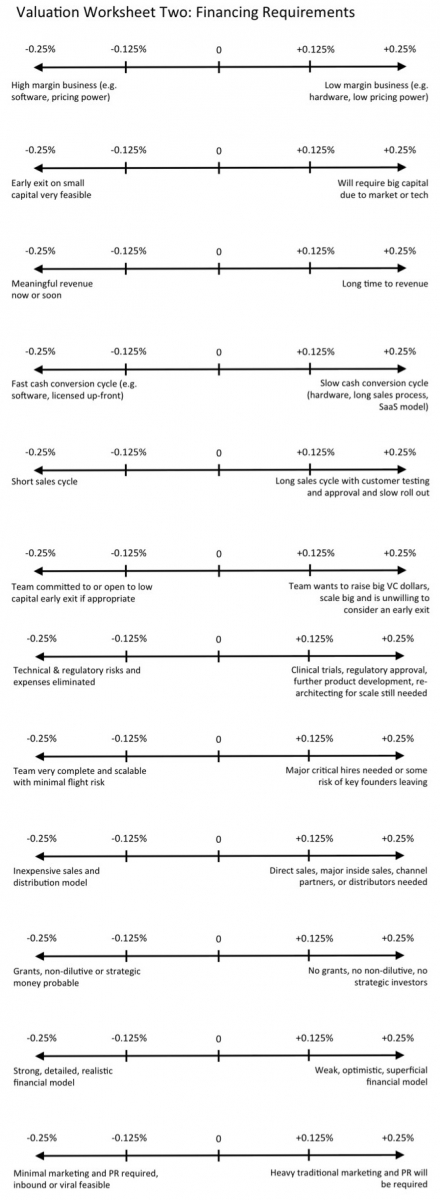

Business Model and GTM: The nature of the business model and planned go-to-market (GTM) is the key factor that will help you ballpark how much additional capital is required. Worksheet Two looks at the key elements of different business models and GTMs and helps you calculate your second set of adjustments - the “Financing Requirements” adjustments - to your valuation. The concepts involved have to do with the cost of going to market, the current state of development, and how quickly the company can convert investments in the business back into cash to help subsidize growth.

If things go according to plan and the company grows wildly, the dilution you experience will be arithmetic (later money comes in on good terms) rather than economic (later money comes in on bad terms). Still, more money required always means more risk and a longer exit timeline. So as a general matter, at the very earliest stages of investing, as a matter of simple economics, you should pay less for deals that have a lot of financing risk and the potential for a lot of dilution. This exercise will help you understand the factors driving this dynamic and create the second set of adjustments to the starting valuation.

Again, for each topic you want to “set the slider” in the right place and tally up your resulting Worksheet Two sub-total to be carried forward. When you boil all the relevant concepts down, here is how it looks (access a downloadable version here):

Now let's transition from the more macro concepts of the first two worksheets to a more micro set of issues in Worksheet Three: Current Deal and Environment.

Want to learn more about the financial mechanics of early stage investing? Download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.