Note: This article is the fifth in an ongoing series on Exits. To learn more about how to plan for exits and maximize returns, download our free eBook today Angel Exits: Perspectives and Techniques for Maximizing Investment Returns or purchase our books at Amazon.com.

How do you know when it’s time? It’s not like a company is a baby that has a 9 month gestation period. Every company is different. Some are ready for a good exit after a year or two of product development. Others might take 10 years or more before they are ready. And many companies go through several potential “exit windows” where they could be sold if they choose. No matter what, you should have an exit plan in place so that when the time is right, you are ready to sell.

Investors need to have realistic expectations on how soon a company will be positioned for an exit. I’ve stopped counting the number of times I’ve heard an entrepreneur state, “Once we hit Milestone A within the next year, there will be plenty of buyers out there.” It’s easy for an investor to be caught in this entrepreneurial hype, but you should be wary and do some research before you accept as gospel the rantings of a novice entrepreneur.

Because each successive plateau in value requires more time, consumes resources and necessitates a bigger buyer, timing an exit correctly will make a big difference in the financial return to the investors and the entrepreneur. If a company misses an exit window, the window may never reopen. So, with the assumption that management and investors are in alignment for the exit, and the company has a solid plan in place, how do you know if the time is right?

Q: What are some key indicators that tell you one of the company’s exit windows is open?

There are many different indicators that a CEO and the board should be looking for when it comes to thinking about exits. In a previous post on successful exits, a number of scenarios are discussed that occur relatively early in a company’s history that will lead to an acquisition offer. Some examples include:

-

A new product that complements a fast growing product line of a large company;

-

A disruptive product that has the potential to damage a larger company’s market position or become difficult to “sell around”;

-

A new product with strategic patents that a buyer cannot risk having fall into a competitor’s hands;

-

A new product that is clearly constrained by lack of sales and that would be instantly accretive and profitable in the hands of a larger sales force.

As part of developing an exit plan for a company, the CEO should have regular relationship-building conversations with potential buyers. Those conversations, and potential strategic partnerships, will provide the board with the insight needed to determine when an exit window is open.

And, as part of these same conversations, the CEO needs to step into the shoes of the buyer and figure out the key milestones that buyers are looking for before they are willing to make a serious acquisition offer. Examples of key milestones might be getting FDA approval for a medical device or building an installed base of 10,000,000 users for a consumer focused startup. As the company is within close range of these key milestones, the exit window starts to open.

Q: What are some of the ways companies fail to capitalize on open exit windows?

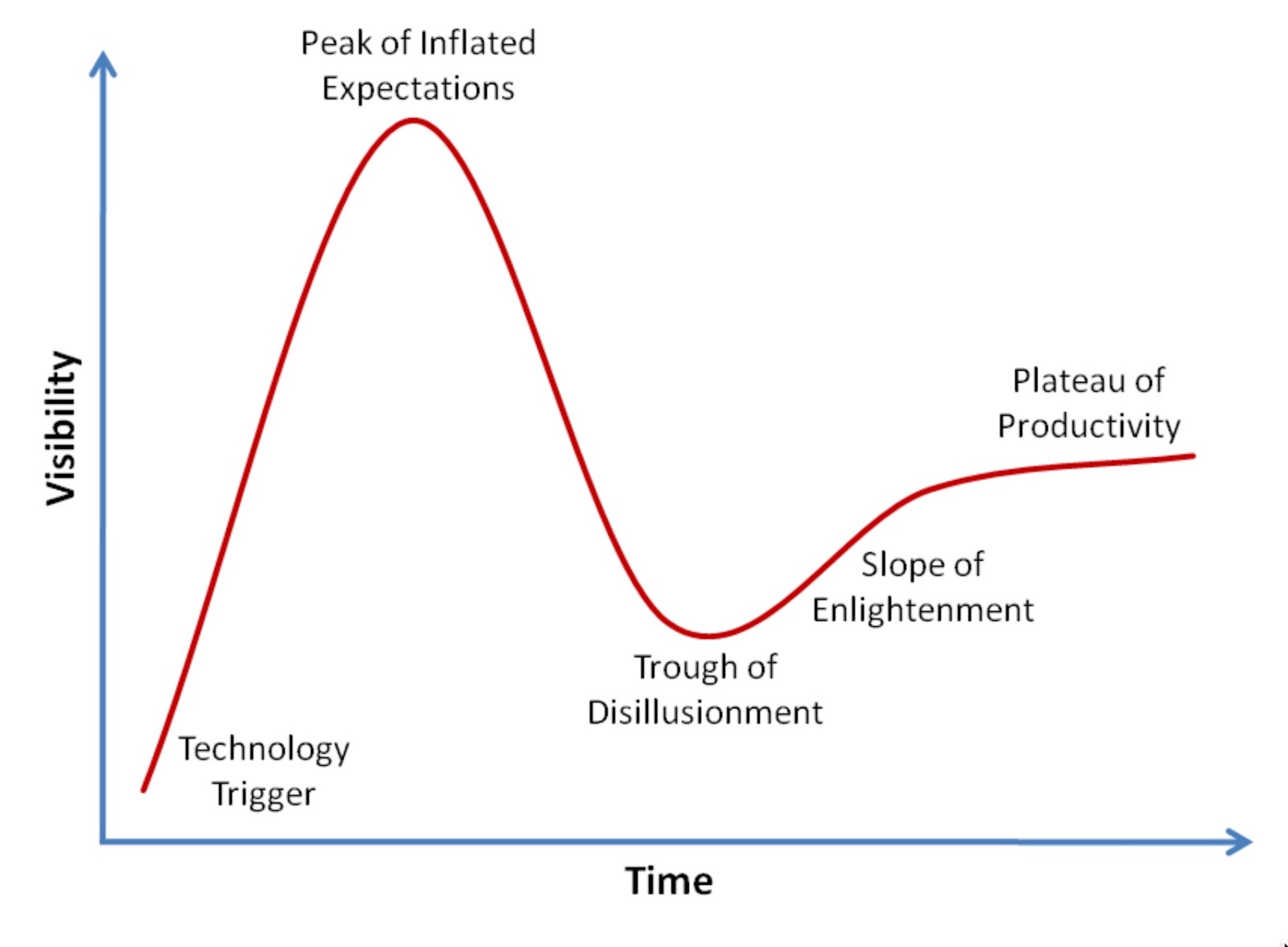

One of my favorite charts is the Gartner Group Hype Cycle graph. The Y Axis on this graph could just as easily be altered to read “Value” instead of “Visibility”. It’s not unusual for a startup in a new market to find itself making critical decisions about its future right at the stage on the chart described as the “Peak of Inflated Expectations”. This is a brief window in time when buyers will overpay for a company, and in fact, might pay more than the company will ever be worth! It is important that all options be considered at that point - too many companies choose monster VC rounds at this point and then have tremendous difficulty and a long path growing back into those valuations as some of the hype deflates.

Failure by a CEO and the board to act on a good exit offer typically occurs for one of the following three reasons:

-

The board doesn’t recognize the offer for how good it is. Almost 5 years ago, Google offered to pay $6B to buy Groupon. Groupon’s board declined the offer. Subsequently Groupon went public. Fast forward almost 5 years later and the value of Groupon based on its current stock price is less than $3B. I am sure there were lots of good reasons for turning down Google’s generous offer, but the shareholders would be better off today if that offer was accepted.

-

The company is not ready to act quickly enough. When a company is focused on getting the business off the ground, not much thought is put into keeping well organized business and financial records. I know of several companies that received legitimate buyout offers that the board wanted to take, but when the buyer asked to see the financials, business contracts, etc, the company didn’t have their ducks lined up. Poor financial records, unorganized customer and partner contracts, lack of board meeting minutes all lead to the acquiring company becoming concerned, asking a lot of questions and reducing the size of their initial offer. And, in a worse case scenario, the buyer decides these clowns are not the threat they thought and takes their offer off the table and buys a competitor instead.

-

There is misalignment with the board and management team. So what is an acceptable buyout offer? If the board can’t agree due to misalignment, the offer won’t be accepted. Make sure you know ahead of time what level of offer is needed to satisfy the majority of investors so you can close the deal.

Q: What about the economy? How does it affect timing for an exit and is there anything you can do about it?

At the macro level, the global economy has a much bigger effect on exit multiples than you might expect. For example, if you look at the returns from VC funds over the past two decades, you will see a direct correlation with the date the fund was raised and the IRR of that fund. Timing plays a big role in how well you do as investor. VC funds that were raised in 1996 and 1997 had a much greater chance of substantial returns to their Limited Partners than funds that were raised in 1999 and 2000.

For this reason, it’s important for the CEO and board to keep in mind what’s going on in the economy at a macro level. This is particularly hard for young CEOs who have never lived through a full business cycle. If you recognize that good times are going to end sooner rather than later, you might want to adjust your exit plans accordingly. That said, we all know that even experienced economists are terrible at predicting what will happen to our economy some time in the future. But what goes up, must eventually come down, and it can pay to listen to the advice of really experienced business people who have lived through many business cycles.

At the micro level, each industry has numerous variables that impact valuations for companies in that industry. Valuations for healthcare companies gyrate wildly as the US Congress debates passing different regulatory and tax laws for the industry. The result is that healthcare startups (which almost always exit through a trade sale) see their valuations rise and fall with the prevailing winds of government regulations.

In addition, when a market segment becomes hot, it’s not unusual to see valuations skyrocket (see Gartner Group Hype Cycle graph above). Witness the explosion in valuations for consumer communication companies such as Instagram, Whatsapp and Snapchat or sharing economy companies such as Airbnb and Uber. But market segments stay hot for a very limited time period. You don’t want to wait around too long before you harvest your investment.

Q: Ham, give us some examples of times when the entrepreneur doesn’t understand how long it will take before their company is ready to be bought?

One area where I see a frequent disconnect between CEO expectations and market reality is in healthcare. Time and time again, I speak with startup CEOs who think they can sell the company early in the testing and development cycle way before it will be ready. This is typical with companies that have to go through regulatory approval such as medical device, diagnostic or therapeutic businesses. Many CEOs believe that once they get through the first, and least expensive, phase of FDA trials there will be acquisition offers from big healthcare companies. Unfortunately, the industry has changed and now most acquisitions occur after the startup takes their product all the way from lab bench through to full FDA approval. That process takes many years and usually 10s of millions of dollars.

The above example is a case where the company stage affects whether the company is ready. There are many variations on this theme, such as the B2B enterprise software company that has great traction in one industry, but needs to show that it can find customers in other industries. Or the consumer internet company that has lots of users but has no clue as to how to monetize those users.

There is another scenario that is quite different from company stage, where a CEO doesn’t understand what’s needed before the company is ready to be bought. We touched on this case in the answer to a previous question. Many CEOs aren’t aware of the expectations that buyers have when they perform their due diligence on the startup company. If you are a B2B enterprise software company with lots of customers, contracts and revenue, you better have your books in order. Acquiring companies will expect to review your financials, so it’s best if you have a recent audit from a well established accounting firm. And, they will want to dig into your customer contracts and any intellectual property materials you have. Keeping your company organized and having a data room ready to go at a moment’s notice is a good best practice for all companies. This requires a fair amount of attention, so the board should advise the CEO to find a resource (e.g. CFO, controller) to oversee this effort. As noted previously, if you don’t have a data room in place when you receive an offer, it can take months to pull one together and the buyer might disappear in the meantime.

Q: What are some of the reasons why companies don’t end up selling their business even when there are interested buyers?

There are lots of reasons, but they all boil down to one primary cause… someone (usually a board member) has the ability to block the sale because they aren’t getting the return they expect. The hope is that if they wait a little bit longer, the company will sell for more. So greed and hubris win out!

If you dig a bit deeper and examine the underlying influences of the primary cause, you will typically uncover one of the following issues:

-

Too much capital was invested in the company, and so the investors can’t get the multiple they need to achieve their financial goals;

-

Since VCs are managing OPM (“other people’s money”) there is a moral hazard - it is extra tempting to wait just a bit longer since they don’t have much, if any, direct personal capital at stake;

-

Expectations for valuation are too high (i.e. everyone is too greedy);

-

Too much competition entered the market and the company isn’t well positioned to command a premium sale price;

-

The company waited until after the exit window starts closing and when the offer comes in they are not ready to move fast enough;

-

The CEO enjoys running the company and is not willing to let someone else take control.

Want to learn more about how to plan for exits and maximize returns? Download our free eBook today Angel Exits: Perspectives and Techniques for Maximizing Investment Returns or purchase our books at Amazon.com.