Note: This article is the eighth in an ongoing series on valuation and capitalization. To learn more about the financial mechanics of early stage investing, download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.

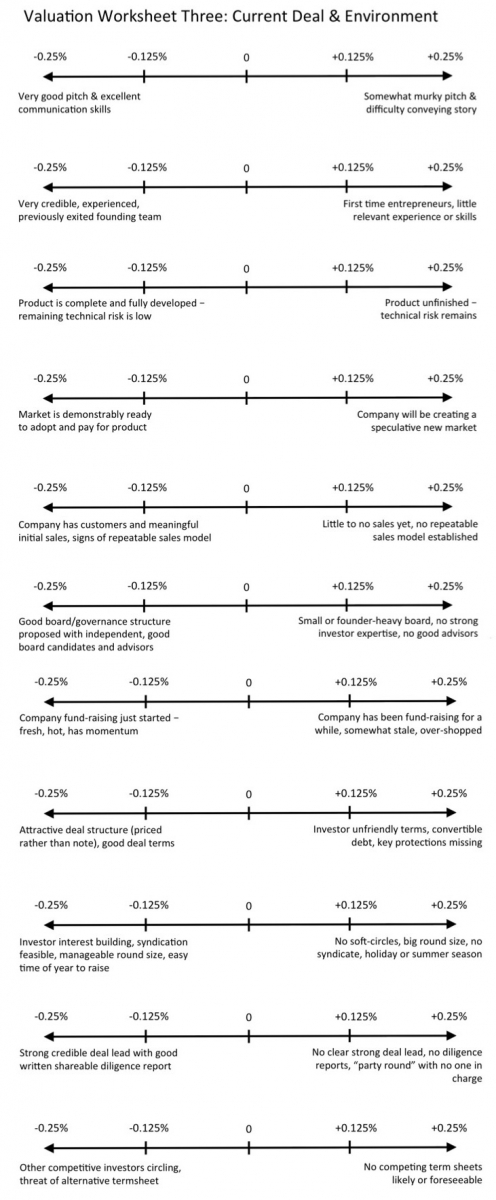

Now we transition from the more macro concepts of the first two worksheets, Exit Practicalities and Financing Requirements, to a more micro set of issues. Worksheet Three helps you assess the relative attractiveness of a particular deal in the real world market context of your market at the relevant moment in time. How many times have you heard someone explain away a deal that couldn’t raise money, or a deal that raised at a seemingly crazy high valuation as “a function of the market” or “what the market will bear”? Investors may like to think we have valuation completely down to a science, but the reality is that market conditions and the relative attractiveness of a company affect the valuation tremendously.

Now we transition from the more macro concepts of the first two worksheets, Exit Practicalities and Financing Requirements, to a more micro set of issues. Worksheet Three helps you assess the relative attractiveness of a particular deal in the real world market context of your market at the relevant moment in time. How many times have you heard someone explain away a deal that couldn’t raise money, or a deal that raised at a seemingly crazy high valuation as “a function of the market” or “what the market will bear”? Investors may like to think we have valuation completely down to a science, but the reality is that market conditions and the relative attractiveness of a company affect the valuation tremendously.

For example, if a hot new company comes along with:

-

A dynamic team,

-

Ready to go in an obvious market,

-

A deal with good terms, and

-

A great board and advisors,

they are going to benefit from a higher valuation.

But if a company has:

-

A team that has been muddling around trying to fundraise for a while,

-

Significant technical or regulatory risk still remaining,

-

Unusual or unattractive deal terms,

they are going to suffer in terms of valuation.

Another factor to consider: the presence or threat of a possible alternative term sheet can have a significant impact on the valuation a deal settles around.

The point is that deals happen in a market. The market conditions and the relative attractiveness of the opportunity are the final set of adjustments you need to make in Worksheet Three before you are ready to settle on your final valuation in the Valuation Look-Up Table.

Below is what Worksheet Three looks like (access a downloadable version here). As with the other two, you need to set the sliders to reflect how the deal scores on the key issues and carry that subtotal forward.

After working through the three worksheets, we move on to the final step of the Seraf Method for valuing early stage companies and bring it all together, applying our adjustments to a valuation starting point.

Want to learn more about the financial mechanics of early stage investing? Download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.