Note: This article is the fourteenth in an ongoing series on valuation and capitalization. To learn more about the financial mechanics of early stage investing, download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.

The first time you receive stock options as an employee is a magical moment. You feel suddenly part of something bigger than just earning a paycheck. You daydream about how various financial scenarios might play out. You take a sudden interest in the wellbeing of your company and the factors which affect its stock price.

The first time you receive stock options as an employee is a magical moment. You feel suddenly part of something bigger than just earning a paycheck. You daydream about how various financial scenarios might play out. You take a sudden interest in the wellbeing of your company and the factors which affect its stock price.

Early in my career I worked with, wrote, and interpreted many stock option programs and thought I understood them very well. Intellectually I did, but that did nothing to prepare me emotionally for being on the receiving end of my first grant of options as I transitioned to becoming a young tech company employee. The sensation of recognition, reward, even worth, has a powerful impact on a young professional.

It is no surprise therefore that startups are nearly universal in their adoption of stock options as a tool for attracting, motivating and retaining new hires. And with all these start up stock option pools everywhere, it is natural for an angel to wonder if they are a relevant part of an angel’s overall investing strategy.

The short answer is yes, in two important ways. First, in connection with setting the valuation of a company, and second as a direct recipient of stock options (or their cousins the restricted stock grant or stock warrant). We have talked quite a bit elsewhere about the impact of option pools on valuation, so here I want to focus on the direct use of these derivative securities on the strategies and returns of angel investors. Let’s see if we can tackle a few of the key questions about options and restricted stock for angels.

Christopher, occasionally, angel investors end up taking board seats or becoming advisors in companies when they make an investment. Should they expect to be paid? What is the rationale for paying them?

There is a long-standing tradition by established companies of paying the independent directors for their board service with equity, typically options or restricted stock. It is viewed as essential for attracting the best talent and compensating them for their time and value-add. And it is believed that using stock that vests over time is a good way to align directors with shareholder interests. If the directors want their compensation to be worth anything, they will focus on mid-to-long term share price appreciation.

With less established startup companies, some of this tradition applies, but with some important caveats. In an established company, much of the board will consist of independent directors who are compensated by the company using some combination of stock and cash. With a startup, the board typically consists of roughly equal parts management and investors, with maybe one independent director mixed in.

How does this affect compensation?

For the management and independent directors, compensation practice is roughly the same: salary, bonus and stock for management and some stock for the independent director. However, the investor component of the board is a bit different for a few reasons:

-

First, they appointed themselves by contractual right,

-

Second, they are already major shareholders, and

-

Third, in the case of VCs, they are already being paid a management fee, and some carry for things like board service. It is their day job.

What difference do those three factors make in compensation?

It tends to weaken the argument that generous compensation is required. For VCs it is hard to force yourself onto a board and then demand that you be compensated with stock. Especially when you are already a major shareholder and your LPs are paying you to do the board work. (Side note: if you are a VC, and you get paid for being on a board, be sure to disclose this to your LPs properly as required by the SECs 2023 reporting rules.)

However, board compensation tends to be a little more generous for angels investors relative to VCs in recognition of several key differences between angels and VCs:

-

The angel is representing and doing the work on behalf of many individual investors;

-

The angel is volunteering her time and not being paid a management fee or carry by any LPs;

-

The angel is likely a much smaller shareholder for whom a few options would make a real economic difference; and

-

The angel is typically helping the company with valuable skills, connections and expertise at a very early stage when help from the board is sorely needed.

How much, and in what form, will this compensation be paid out to the director or advisor?

Payment is almost invariably in the form of equity rather than cash. Paying directors cash would be a terrible use of that scarce resource early on, and also a lost opportunity for alignment with shareholders. The form of equity paid is usually either stock options vesting over time, or increasingly, restricted stock where the restrictions lapse over time. The typical approach is to give an initial grant at the time of joining the board, and then do supplementary grants annually or once every couple of years.

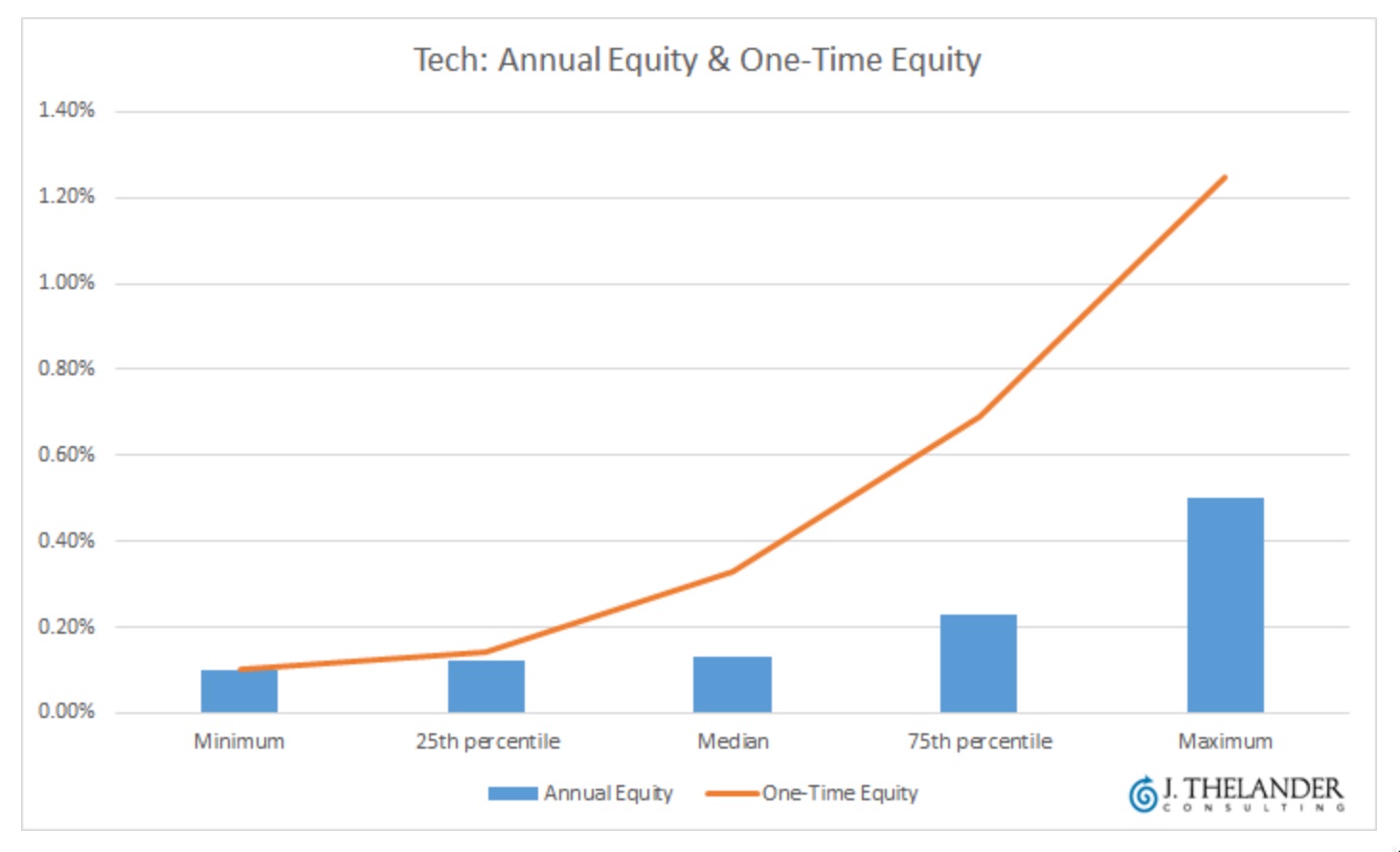

In our experience, early-stage directors are typically given an initial grant in an amount equal to somewhere between 0.25% and 1.0% of the company’s total shares outstanding on a fully diluted basis. Board chairs or extremely active directors with specific industry contacts and introductions may be at the higher end of the prevailing range. Executive directors and special advisors are special cases and may fall outside of the range. It is the responsibility of the board to ensure the appropriateness of all compensation paid by the company. Assuming a grant is appropriate, it may have a very big impact; for an angel investing their own money in order to buy a likely similar or lower percentage of the company, a grant like that can be a huge multiplier on your returns - doubling or even tripling a good outcome.

Subsequent supplementary grants would be at the lowest end of that spectrum. Based on market studies, our experience of how angel directors are paid would appear to be fairly consistent with prevailing market norms for non-investor directors; Pitchbook has done a study and come up with pretty similar findings:

For more detail on the other considerations to keep in mind when designing or dealing with director compensation, we’ve done a thorough overview of the issues and pitfalls.

So options and restricted stock have big potential for angels sitting on boards. Are there tax issues a board member should take into consideration with the stock compensation they will receive for their service to the company?

In a word, YES!

The key threshold issue is to consider the form of equity security. Stock options and restricted stock are economically quite similar, but have very different mechanics and therefore very different tax considerations. Restricted stock is increasingly used instead of options because of its greater tax efficiency.

With options, you are being granted a right to buy a certain amount of stock for a certain price at certain time(s) in the future. You do not own the stock until vesting occurs and you exercise the stock option. You pay nothing up front, but you do not own any stock either.

Restricted shares are granted up front, but subject to restrictions which fall away over time. In other words, options have ownership rights which vest over time, and restricted shares have ownership restrictions which lapse over time.

What is the key difference between stock options and restricted stock?

They are really very similar in their ultimate effect; the key difference is the tax efficiency. Restricted shares allow the recipient of the shares to recognize and declare the imputed income from the transfer of restricted shares on day one. That allows the director to make an election under IRS Section 83(b) and pay a small amount of income taxes up front (reflecting the current fair market value of stock that is subject to restrictions). And, under the 83(b) rules, pay the lower capital gains rate on any future profits, including potentially the lower long term rates for stock held for the requisite period. For more on working with 83(b) we’ve put together an entire toolbox of forms and information.

Because directors are not employees, the options they get are called non-qualified options. With these non-qualified stock options, all the ownership timing is compressed. To take advantage of capital gains treatment, you must:

-

Wait for the stock to vest,

-

Then pay the exercise price,

-

Then pay tax on any income that is imputed from the difference between your exercise price and the fair market value at the time

-

And then begin your holding period for capital gains treatment.

Suffice it to say, restricted stock is a lot less work - a one time tax payment up front rather than a tax payment each time options are exercised. And, because restricted stock allows you to get that capital gains clock running, it may also allow you to leverage lower tax rates.

Because non-qualified options are so much more work, most option grantees just end up holding onto options and doing a cashless exercise at the last minute (e.g. at the time of company exit or on the eve of option expiration - typically ten years). They use some of the profits to satisfy the exercise price and just dispose of the whole bundle of options at once. Of course that means they are going to pay ordinary income tax rates on the whole transaction.

So if you don’t get restricted stock, you end up with Non-Qualified stock options. What are some important considerations when exercising your stock options?

With options, once they vest, you must first decide whether you are even going to exercise the option before the time when you are ultimately forced to (by exit or expiration). Then you must decide if you are going to sell the shares immediately or hold on to the shares you just exercised.

If you exercise and sell them immediately (assuming that is permitted under the terms of your investment and there is a market for the shares - remember we are talking about private companies here) then you will pay:

-

The exercise price and

-

Taxes at ordinary tax rates on the difference between your exercise price and the Fair Market Value (FMV) at the time of exercise.

This is true for both qualified employee shares and the non-qualified shares a board director would get.

If you exercise and sell the shares immediately, all the income is deemed compensation (ordinary income) for both types of awards. So for example:

-

If you have 10,000 options at an exercise price of a $1 and the FMV is now $5,

-

If you exercise the options you will pay $10,000 to the company to exercise them and pay taxes (at ordinary rates) on $4 of difference per share or $40,000 in profit.

-

That could cost you approximately $12,000 of taxes.

-

So the take home amount after selling your shares for $50,000, less the cost of $10,000 for the exercise, less $12,000 of taxes, is a figure of $28,000 in net profit.

An option is a pure upside play. Fortunately you don’t have to commit to paying the exercise price on your options until you see whether the options are profitable. Initial instinct would dictate holding onto them and deciding as late as possible whether you want to exercise. However that instinct runs into direct conflict with tax considerations.

It may seem counter-intuitive, but tax advisors often tell clients to exercise the options as early as you dare. If you can afford the exercise price, and you are willing to take the risk of paying good money for illiquid private company stock that might be worthless, then exercising early allows you to do two important things from a tax efficiency standpoint:

-

First, you can exercise when fair market value (FMV) is still low and the per share “spread” or profit is small so the ordinary income tax bill will be small.

-

Second, it allows you to get the capital gains tax clock running on those shares so that you can hopefully qualify for long term capital gains before you are forced to sell as part of a company exit scenario.

What does this mean in dollar terms? Let’s look at an example:

-

Suppose you have options with an exercise price of $1, and the FMV is $5.

-

If you think the company is poised to take off or do a financing soon, then you may take the view that FMV is relatively low in the grand scheme of things and want to exercise the options.

-

You will pay taxes on the $4 spread. And then you will start holding the stock for capital gains holding period purposes.

-

If the company takes off and is acquired for $15 a share, you are going to be very glad that you get to apply the capital gains tax rate to $10 of the total $14 in profit rather than ordinary income tax on all $14.

On the other hand, if the company is struggling a bit and is clearly going to need some time before it qualifies for a real up round, let alone a great exit, you might decide to hold off a bit and not let the “tax tail wag the dog.”

If the company is struggling, that means future value increases are still speculative and the risk of failure looms large. In that case, taking hard-earned after-tax money and using it to pay the exercise price to purchase and hold sketchy private company stock, does not make much sense. In this scenario the loss risk is greater than the tax efficiency risk. Better to wait a little while for the situation to come into focus and take your chances that you will still be able to exercise in time for a good FMV spread and a long enough capital gains holding period.

Are there any other issues that stock option holders need to consider?

One other thing to keep in mind at all times is that all the options have an expiration date. Many option plans at companies specify a ten year life, and you don’t want to be forced into acting quickly. Never a bad idea when you get options to set a calendar reminder (or a Seraf account reminder) for 15-18 months before the final expiration date so at a minimum you can just punt and exercise at the last minute and still get at least a one year capital gains tax holding period.) It is a shame to forget about this issue and lose the benefit of a well-thought out execution strategy.

Also, remember the above relates to non-qualified options; for more on the rules applicable to employee incentive stock options, see this piece done in conjunction with our advisors at KN+S.

So that covers 83(b) elections on restricted stock and capital gains treatment on option exercises. Are there other issues to be mindful of in a positive outcome situation?

Yes, there is one other major tax issue you want to be aware of, and that is the considerable benefit available under IRS Section 1202. This part of the US tax code introduces not only huge potential savings, but also really long five year holding period requirements which affect your option exercise timing considerably.

Section 1202 deals with a gain on a stock sale. If your investment qualifies for 1202 treatment, up to 100% of the gain could be excluded up to the greater of $10,000,000 or 10 times your investment. To qualify, this stock must

-

Be a domestic C Corporation from inception;

-

The gross assets of the Company must be under $50 million at the time the investment is made; and

-

The stock must be issued for either cash, property, or services.

-

Additionally, the company must be an active operating business (i.e. not an investment business or one similar to a service business such as a law firm.)

-

And finally, you must have held the stock for at least five years. Collectively, these requirements are the QSB or Qualified Small Business test. If your stock meets all these tests, it is QSBS or Qualified Small Business Stock.

Under 1202, the percentage of your gain you are allowed to exclude depends on when you acquired the qualifying stock. As long as you hold your stock for a minimum of 5 years before the sale occurs, your capital gains exclusion is calculated as follows:

-

Acquired between 8/10/1993 and 2/17/2009: 50% Exclusion

-

Acquired between 2/18/2009 and 9/27/2010: 75% Exclusion

-

Acquired after 9/28/2010: 100% Exclusion

But 1202 does have a few catches that many people are not aware of. If you held convertible debt early on in a company and then it converted into stock later on, the period during which you held the note does not count toward your 1202 five year holding requirement; that clock starts when you convert to equity (though the note period does count toward your long term cap gain determination). And you need to keep in mind that other measures don’t tie back, such as the $50 million in assets test, which is tested at the date of conversion of the debt to stock.

Another thing to know is that if you own 1202 QSB stock, and then decide to gift it to another individual later, the stock will retain its character of 1202 stock to the donee. Thus a parent who owns 1202 stock can gift it to his or her children, and they can benefit from the same reduced capital gains exclusions that the parent would have.

A final point: these 1202 rules are quite complicated and subject to change and their applicability to your situation may depend on the particular details of your investment, so it is best to get help from professional advisors before making assumptions.

From time to time I receive warrants as a part of an investment. What are they and when is the ‘right’ time to exercise warrants?

Warrants are basically identical to non-qualified stock options from an economic and tax perspective. The only difference is that warrants are typically one-off instruments and not issued under the terms of the stock option plan (though they may or may not use shares set aside in the option pool.) Options are commonly used as compensation for employees, directors, advisors and consultants, and warrants tend to be used more frequently in business transaction contexts. For example, warrants might be issued to a bank in connection with taking out a line of credit, or might be included in an investment deal as a sweetener to encourage investors to jump into the first close or to help span a gap in valuation expectations. One cosmetic difference between options and warrants is that warrants have all of their terms in the warrant document, whereas option agreements usually rely on having some terms spelled out in the umbrella option plan documentation.

In terms of exercising warrants, the analysis is similar to a non-qualified option. Generally speaking, the best strategy for exercising warrants is to wait until you are sure the company is pretty well out of the woods (and the warrants will therefore likely be worth something) and then, once you have made that determination, exercise them as soon as possible to start the capital gains clock running. By doing the exercise early you are hoping to get at least a year of ownership before any acquisition occurs. That way they are treated as long term capital gains with a preferential rate, as opposed to short term capital gains, which are taxed at the same rate as ordinary income. Put another way, you want to exercise them as soon as you reach the point that you are sure you are going to exercise them.

So why not just exercise them right away? Because you have to spend money to exercise them. If the exercise price is fair market value (FMV) at the time they are granted, that can still be real money - equivalent to simply investing in the company at that price. If the warrants are issued way below FMV, say for a penny each, then you might as well exercise them right away.

For a bit more on warrants, including tracking of exercise dates, see this post on Stock Warrants: Sweetening the Deal for Angel Investors. Next up in this series: Seraf Toolbox: Capitalization Tables with Waterfall Analysis.

Want to learn more about the financial mechanics of early stage investing? Download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.