Note: This article is the fourth in an ongoing series for angels new to investing. To learn more about building an angel portfolio, download this free eBook today - Angel 101: A Primer for Angel Investors or purchase our books at Amazon.com.

Angels dealing with entrepreneurs in both the coaching and the evaluating context are often confronted with the question of what materials are appropriate for each stage of engagement. This is one of those situations where it doesn’t pay to be creative. There are norms both in terms of what documents to have and in terms of how to prepare them, and adhering to those norms is in your a company’s best interest. Trying to innovate and create something different will be an exercise in frustration for you and your readers.

Angels dealing with entrepreneurs in both the coaching and the evaluating context are often confronted with the question of what materials are appropriate for each stage of engagement. This is one of those situations where it doesn’t pay to be creative. There are norms both in terms of what documents to have and in terms of how to prepare them, and adhering to those norms is in your a company’s best interest. Trying to innovate and create something different will be an exercise in frustration for you and your readers.

Christopher has invested in a ton of startups, coached 100 times more startups, and taught, written and spoken on this subject extensively, so let’s see what he has to say about it.

Q: Christopher, when advising an entrepreneur, what should you tell her are the key documents she should have when setting out to raise money?

At the beginning, there are really only two documents you need (ok, three - one of them you need two versions.) Those documents are an executive summary and a slide deck. With the slide deck, you need two versions - a more text-heavy version which can be emailed, read and understood without you there to explain it, and a more spare visual version intended to be used as a backdrop to a live discussion. Sending anything more than this during an initial contact with investors is just a waste of time - even an interested investor won’t read it.

Q: If they have a slide deck, why do they need an executive summary?

As I have explained in detail elsewhere, an executive summary serves several key purposes:

-

It provides a condensed quick reference guide to a business in a format the typical investor is going to find familiar.

-

The extremely “boiled down” format is a chance for an entrepreneur to demonstrate both the clarity and completeness of her thinking as well as her communication skills.

-

It is a piece of "collateral" that an investor can easily share and use to discuss a company with other investors and solicit their input. It reduces friction by saving investors the trouble of having to re-summarize the company themselves, while keeping the entrepreneur’s original description intact.

-

It gives time-pressed readers an easy way to quickly absorb the concept of a business vs. having to read many pages of a business plan.

People sometimes question the value of the short executive summary when they also have a slide deck, but it really is essential. Investors absolutely need a one-pager to start with. They will also need a slide deck, but the one-pager must be present. Why? For three important reasons:

-

The process and discipline of preparing a very good one page executive summary will clarify and tighten an entrepreneur’s thinking. The process of writing it will make them far more cogent in talking about their business—both in person and when using their presentation deck.

-

Different people learn different ways - some people are speed readers who want to skim super condensed material and other people are visual learners who really get it only when they have seen a picture.

-

The executive summary is an insurance policy. Slide decks can take a lot of concentration to work your way through and ferret out key answers. Having a quick glance overview of the business concept as an easy path to engagement is much more accessible for busy skeptics.

Q: What should be in this executive summary?

The executive summary should include most of the same topics from a basic slide deck, but the details must be tightly packaged and sparingly-worded to fit on one page, or at most, the front and back of a single sheet. The typical format includes a box on the right with the company name, logo, URL, number of employees, key players and advisors and important investors. Along the bottom of the page a short, wide box shows at-a-glance financials: gross revenues, expenditures and net for the current year and the next 3-4 years. The middle of the page includes short 200-400 character paragraphs on the following topics:

-

One Line Pitch

-

Business Summary

-

Management Team

-

Customer Problem

-

Product/Service

-

Target Market

-

Customers

-

Sales/Marketing Strategy

-

Business/Revenue Model

-

Competitors

-

Competitive Advantage

The one-page executive summary isn’t easy. In fact, entrepreneurs may get incredibly frustrated trying to boil down their big idea into only one data-intensive page. But the discipline of doing it and figuring out how to pull all the key answers into one place is really valuable. Insisting that entrepreneurs take the time to do it properly is not only going to serve them well, it will serve you well too.

Q: OK, what about these two versions of my slide deck?

As noted above, you are really looking to have two versions of the same deck. Think of one version as the “email deck” and the other version as the “presentation deck.” The difference is that the email deck can be read and understood without the entrepreneur there to explain it. Whereas the presentation deck is spare, bold and visual and does not have a lot of distracting text to pull the audience’s attention away when they should be listening to the entrepreneur. Companies frequently get these two decks mixed up or just blend them together to keep from having to update two decks, but that is a mistake. For a deck to be maximally effective, it has to be designed for the purpose it will serve - reading or live presentation.

A deck should be about 15-20 slides and the presenter should know it well enough to be able to pitch it smoothly in as few as 10-15 minutes. In some more interactive cases there might be more time, but the presenter should practice and be able to pitch it well in both a 10 minute pitch and a 15 minute pitch.

Both versions of the deck should contain the same basic material:

1. Customer Problem: description of customer pain and how the company solves it - concept & key elements

2. Product Overview: what the company does, for whom and why it’s compelling

3. Key Players: founders, key team members, and key advisors, with industry backgrounds and expertise

4. Market Opportunity: market size, growth characteristics, segmentation

5. Competitive Landscape: competitors and competitive feature sets, plus sustainable competitive advantages

6. Go-To-Market Strategy: how the company will sell its product, in detail, including roughly how much it will cost to build that sales engine

7. Stage of Development: product development, customer acquisition, partner relationships

8. Critical Risks & Challenges: what can go wrong and how the company plans to manage it

9. Financial Projections: how much time and money it will take to get to cash flow break-even and five year projections (it is really helpful if entrepreneurs show Yr5 mid-case, worst case and best case with key assumptions)

10. Exit Options: categories of likely buyers, rationales, list of specific likely buyers and comparables with valuation multiples

11. Funding Requirements: how much, what the company will use it for, what milestones it expects to hit.

That’s about it. If there is additional information or illustrations that might be essential to telling the story, put them into an appendix and the presenter can jump to those slides as needed. But for the main part of the deck, it should cover those 11 topics with a maximum of 1-2 slides per topic. Trying to cover much more in a basic deck is a mistake. Investors will lose the forest for the trees and get stuck in minutiae. At this stage, it is about the forest - details can be drawn out during subsequent Q&A or during subsequent due diligence.

Q: How should a deck be constructed? Is there a standard template somewhere?

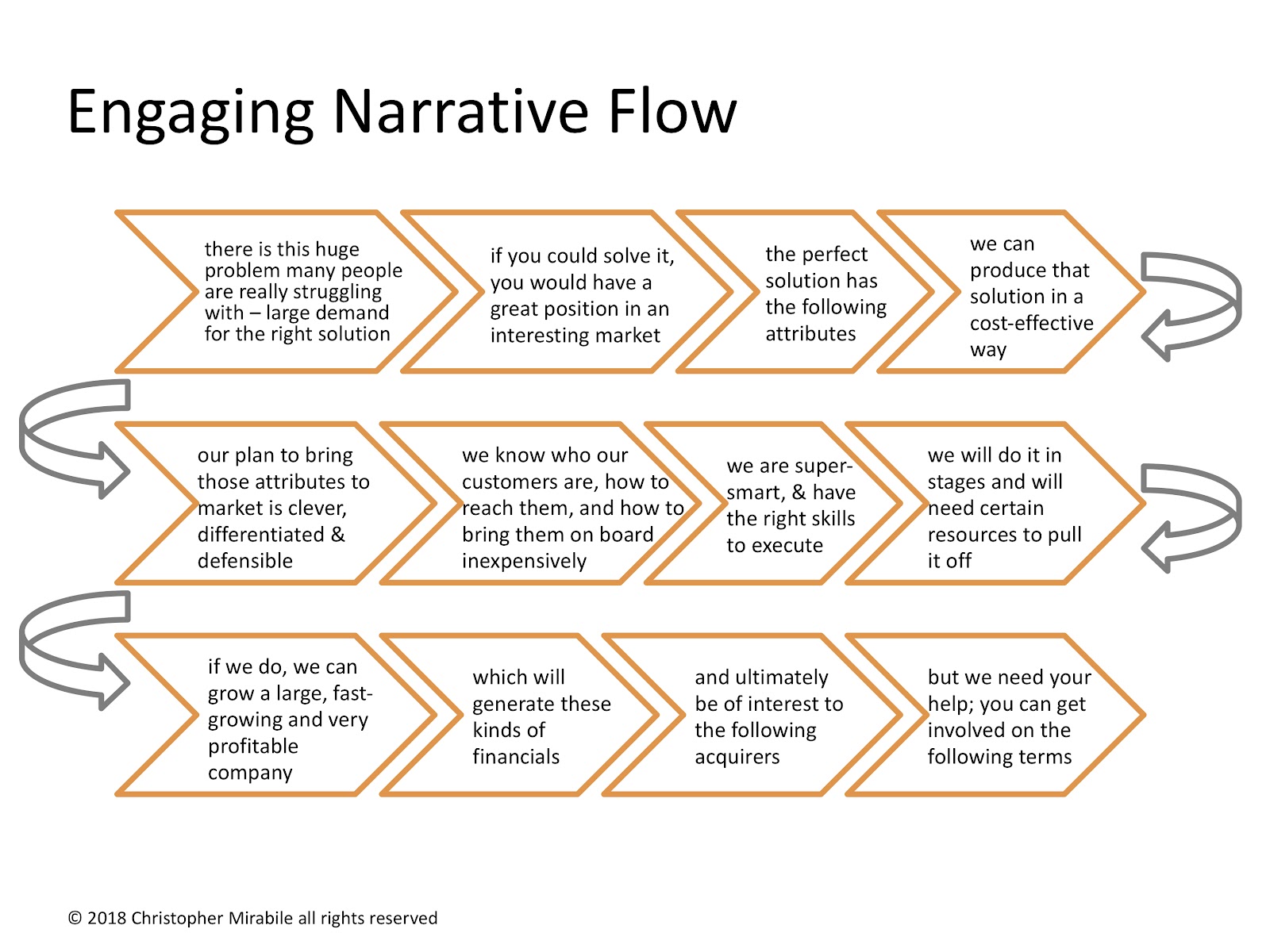

This is where there is probably some room for creativity, but again, I would not go too wild. As long as the deck covers the 11 key topics, and it’s pitched it in an engaging way, the presenter can probably make any order work reasonably well. That said, over many years of sitting through pitches and coaching on how to build good decks, I think there is a conceptual story flow that works pretty close to universally. I recommend most entrepreneurs start with it and then make changes only if they feel it is necessary for the effective telling of their story. Here is what that concept flow looks like. Note the slides are not supposed to say exactly what is in the boxes. That text is there to help understand the narrative arc the presenter is trying to convey:

The key to this formula is it covers all the required subjects, but strings them together into a coherent and engaging narrative flow. Entrepreneurs need to cover all the building blocks, but the key is in the arrangement of those blocks.

The astute may have noticed that a discussion of team does note come first. Most investors say the team is the most important thing, and I agree, so some people recommend that entrepreneurs start with the team. They are wrong. You are trying to craft a narrative here, and starting with the team’s qualifications just is not an interesting place to start. Hook the audience with the story of the customer and the problem. Team is important, but as you can see from above it comes later in the flow.

Q: Other tips on making the deck great?

Yes; three words: visual presentation matters. When constructing a deck, visual ugliness is a completely avoidable sin for which there is no excuse. If the entrepreneur is worried she has no taste or cannot judge visual designs well, get a graphic design acquaintance to help de-uglify the deck. Clip art, jaggy images, lime green fonts on a black background - these are the hallmarks of the un-funded.

Further, most people don’t realize that visual presentation of numerical and complex data matters enormously and can make or break your ability to land your point with impact. Take time to come up with innovative and impactful ways to present numerical and complex data. Consider the power of things like same size analysis and rounding that allows the reader to pull insight from previously impenetrable numbers. But be disciplined: every chart and graphical element must add impact to the story without adding clutter or distraction or ugliness.

Q: What about a detailed financial model and a full length business plan? Don’t entrepreneurs need those at the pitch stage?

They need them in order to do a good pitch, and they will need the model and some parts of a detailed business plan immediately after the pitch. But these things are not part of the pitch. The detailed financial model is a key part of the due diligence process, and investors will want to dig into it and look at the assumptions and the detail, but it is not part of the pitch.

Similarly, a big MBA style business plan may have a lot of value for planning and analysis purposes, but it is just that - a planning document, not a communications document. As Eisenhower said, “plans are worthless, but planning is everything.” You should not email an 80 page business plan around - first, because no one will read it and second, because it makes you look naive and uninformed about the startup fundraising process.

Q: What about preparing for a deep dive and having other diligence materials?

For more detail on the key diligence items the entrepreneur needs immediately after getting investors to bite the hook on their pitch, here is an article that contains a detailed diligence checklist explaining both the documents and the key tasks and questions with those documents.

For some help preparing for and surviving those first deep dive meetings, here is a mini-series on the topic:

Prepping for a Deep Dive Meeting with Investors

How to Survive A Deep Dive Meeting

Avoid These 5 Deep Dive Meeting Pitfalls

As you can see, there is some complexity to this topic. At a high level, it is not that complicated. All that’s needed to have is some basic information about the business opportunity. But when you scratch the surface, it becomes clear that the form in which that material is presented matters. How it’s rolled out matters almost as much as the content. really needs to lead with big concepts and big ideas to allow people to latch on without a lot of distracting clutter in the way. And, have to be ready at a moment’s notice to demonstrate they have command of the details and have thought them through.

It’s a tall ask and it may sometimes feels unfair. An entrepreneur may only need to be good at this for a few key moments of their career, but when they need to be good at it, they really need to be good at it. he reality is that this boils down to a test of very basic leadership skills; if the entrepreneur can think and communicate in a clear, organized and compelling fashion and with an empathetic eye towards how their audience needs to consume what is said, they will do just fine at pitching their opportunity.

Want to learn more about building an angel portfolio and developing the key skills needed to make great investments? Download Angel 101: A Primer for Angel Investors and Angel 201: The 4 Critical Skills Every Angel Should Master for free, or purchase our books at Amazon.com.