Note: This article is the second in an ongoing series on valuation and capitalization. To learn more about the financial mechanics of early stage investing, download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.

Several years ago, I was speaking to a colleague of mine. He was trying to decide between two great job offers, and was having a difficult time making a final decision. When I asked him questions about work environment, the quality of his co-workers and boss, and the future potential for the companies, he responded that both companies fit what he was looking for.

Several years ago, I was speaking to a colleague of mine. He was trying to decide between two great job offers, and was having a difficult time making a final decision. When I asked him questions about work environment, the quality of his co-workers and boss, and the future potential for the companies, he responded that both companies fit what he was looking for.

Next, I started asking about his compensation package. For salary and bonus, the two companies were equivalent. However, when it came to stock, there seemed to be a big difference. One company offered him 25,000 shares that vested over a 3 year period. The other company offered 300,000 shares that vested over 4 years. Because one offer was almost twelve times greater than the other offer, my friend felt he should take the job from the company that was giving him more shares. His decision was a pretty typical response from someone without much financial experience.

So I asked him a simple question. “Do you know how many shares each company has issued?” His face went blank and he shook his head ‘no’. He had no clue what I was talking about. I paused for a minute and then asked my question in a different way. “Do you know how big a slice of the company pie you are getting from Company A vs. Company B?”

Now I could see the wheels turning in his head. “Ahh, I get it”, he replied. “I don’t know the answer to that question, but I will ask each company and get back to you with the answer.” The next day he texted me and told me that the 25,000 share offer was equivalent to a bit more than 1% of the company’s total outstanding shares. The 300,000 share offer was about a half percent of that company’s shares. So even though one offer looked very generous compared to the other, in reality, the smaller share offer represented more than twice the ownership position of the bigger share offer.

I tell this story as one simple example of the importance of actually understanding a company’s Capitalization Table (“cap table”) before transacting in their shares. Shareholders who don’t have a good grasp of this important investment concept are at a significant handicap when it comes to investing. If you don’t know what you own, how can you understand either its value today or its potential value in the future?

Ham and I spend a lot of time thinking about cap tables, making sure we understand what our ownership position will be after we invest in a company. Furthermore, we spend time modeling future cap tables for our investments, helping us understand what happens over time as companies raise additional rounds of financing. Let’s ask Ham for a little more about the basics of this so you can wrap your head around what we consider to be one of the most important concepts of early stage investing.

Ham, to start out, what is a Cap Table? Can you give us a simple definition?

Whenever I hear the term “cap table”, I can’t help but envision an accountant wearing a green eyeshade hunched over a giant ledger. In this ledger is a listing of all the shareholders and security holders in the company tallied up to make sure that the company’s share count equals the total number of shares held by the sum of all the investors and other security holders such as managers, founders, paid advisors and employees. In summary, that’s what a cap table represents - it is a table illustrating the capitalization of the company.

To be a bit more specific, the cap table tracks the equity ownership of all the company’s shareholders and security holders and the value assigned to this equity. In case it is not clear, cap tables need to be comprehensive. They should include all elements of company stakeholders such as convertible debt, stock options and warrants in addition to common and preferred stock.

Typically built and stored in a spreadsheet, the cap table is one of the most critical documents maintained by the company. I can’t stress enough the importance of accuracy with this document. I highly recommend that an investor spend some time reviewing the company's cap table and making sure their ownership position is fairly represented. If it isn’t, you will need to reach out to the company and make sure any appropriate corrections are made in a timely fashion.

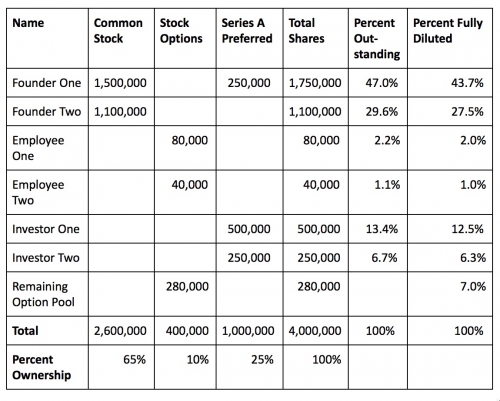

Since we are talking about numbers, I think it helps to see what a basic cap table looks like. Here is a very simple example:

The table above highlights the most basic information in a cap table. For example, if you are Investor One, you own 500,000 shares of Series A Preferred stock. The company has the right to issue up to 4,000,000 shares including the option pool, so on a fully diluted basis (i.e. pretending all the options were granted), your holdings are equivalent to 12.5% of all the shares of the company.

To help you get started modeling a company’s cap table, we’ve provided two examples you can copy and experiment with. These spreadsheets will help you model single round and multi-round financings and include features such as options, liquidation preferences, participating preferred and the resulting waterfall analysis.

What are the key terms used in cap table analysis that every investor must understand?

If you want to be an effective investor, it’s important for you to be able to speak fluently the language found in a cap table. To get you up the curve faster, we’ll break the key terms used in cap tables into three categories: Valuations, Security Types and Share Counts.

Valuations

-

Pre-Money Valuation - This is the valuation placed on the company prior to an investment made in the company. This valuation is typically set through a negotiation between the investors and company management. We discuss how this valuation is set in great detail in later articles.

-

Post-Money Valuation - This is the effective valuation of the company after an investment is made in the company. For example, if the pre-money valuation is $3M and the investors make a $1M investment, the post-money valuation is $4M (the $3M value plus the $1M in liquid cash now on the balance sheet).

-

Price per Share - This is a calculation based on taking the post-money valuation and dividing it by the number of fully diluted shares. If we have a $8M post-money valuation and we have 4 million shares, the price per share is $2.

Security Types

-

Common Stock - The most basic form of equity ownership in a company is called common stock. Each share of common stock represents partial ownership of the company and gives the shareholder certain rights to company profits and voting on corporate matters, all as spelled out in the charter and the law of the state of incorporation.

-

Preferred Stock - A class or series of stock with special rights and privileges outlined in the company’s charter. By default, preferred stock is typically paid before common (but after debt) in a liquidation or sale situation.

-

Convertible Preferred Stock - This is preferred stock which has the option to convert to common stock (and be paid at the same time and rate as common) under a specified set of circumstances, including at the holder’s discretion.

-

Participating Preferred - This is a type of preferred stock which has the right to be paid some multiple of the original purchase price (e.g. 1X) and then also convert to common stock and “participate” in the distribution to common as if it had simply converted in the first place.

-

Non-participating Preferred - This is a type of preferred stock which has the right to be paid some multiple of the original purchase price (e.g. 1X) OR convert to common stock and “participate” in the distribution to common. The investor will choose the liquidity method that delivers the greatest financial return. This can also be referred to as just “preferred stock” but calling it “non-participating preferred” avoids all doubt about what kind it is.

-

Stock Options - A stock option is a contractual right to purchase a specified number of shares for a specified price at a specified future date or dates. Stock options are typically issued under the terms of a stock option plan out of a pre-approved pool of shares set aside for options and restricted stock grants.

-

Warrants - Warrants are nearly the same as options in that they are a contractual right to purchase a specified number of shares for a specified price at a specified future date or dates. Unlike stock options, warrants are typically one-offs and not issued under the terms of the stock option plan, though they may or may not use shares set aside in the option pool. Options are commonly used as compensation for employees and warrants tend to be used more frequently in business transaction contexts.

-

Restricted Stock - Restricted stock is increasingly used instead of options because of its greater potential tax efficiency. With options, you do not actually own the stock until vesting occurs and you exercise the stock option. Restricted shares are granted up front, but that up-front ownership is subject to restrictions which fall away over time. In other words, options have ownership rights which vest over time, restricted shares have ownership restrictions which lapse over time. The key difference is tax efficiency - restricted shares allow the recipient to make an election under Section 83(b) and pay a small amount of taxes up front in order to access the lower capital gains rate on any future profits.

Share Counts

-

Authorized Shares - all shares in a company must be properly authorized before they are issued (as in the context of a financing). Authorized shares refer to that number of shares which has been duly authorized by the company’s board for present or future issuance.

-

Outstanding Shares - This is the total number of shares which have actually been issued. It does not include options which have not been granted, nor does it include granted options which have not been exercised, since the shares are only issued upon exercise.

- Fully Diluted Shares - This is a calculated number which models all granted options, restricted stock, warrants and often the remainder of the option pool itself into one single number of shares that represents the theoretical count if all outstanding contingencies were granted and exercised.

For more on understanding early stage capitalization tables, continue on to Part II of Who Owns What - Understanding Early Stage Capitalization Tables.

Want to learn more about the financial mechanics of early stage investing? Download this free eBook today Angel Investing by the Numbers: Valuation, Capitalization, Portfolio Construction and Startup Economics or purchase our books at Amazon.com.