Note: This article is the seventeenth in an ongoing series on venture fund formation and management. To learn more about managing a fund, download this free eBook today Venture Capital: A Practical Guide or purchase a hard copy desk reference at Amazon.com.

In Part I of this article, we discussed the two key components of compensation in a venture fund - management fees and carry - and what level of capital commitment LPs expect from GPs. In Part II we looked at historical VC fund metrics, what kind of returns LPs should anticipate from a venture fund, and some ways to improve the rate of return. Now let's address venture fund costs and expenses, and the total level of compensation a VC can make running an early stage venture fund.

In Part I of this article, we discussed the two key components of compensation in a venture fund - management fees and carry - and what level of capital commitment LPs expect from GPs. In Part II we looked at historical VC fund metrics, what kind of returns LPs should anticipate from a venture fund, and some ways to improve the rate of return. Now let's address venture fund costs and expenses, and the total level of compensation a VC can make running an early stage venture fund.

What are some of the costs associated with running a fund and who pays for these organizational expenses?

The annual management fee for a venture firm is designed to be used to pay the operational expenses associated with running the fund. These expenses include some or all of the following items:

-

Salaries and benefits for the GPs

-

Salaries and benefits for other employees (e.g. venture partners, analysts, office managers, CFO, etc.)

-

Rent and operating expenses for an office

-

Marketing programs to raise the visibility of the fund to entrepreneurs, syndicate partners and LPs

-

Legal and accounting fees

-

Travel related to sourcing deals, attending board meetings and industry events

-

Annual meetings to keep your LPs informed and engaged

-

Software (e.g. portfolio management, CRM, accounting)

So that 2% management fee has a lot of mouths to feed and bills to pay. All those expenses can make a $1M management fee from a $50M fund not seem so lucrative after all! As a side note, in the process of forming a new fund, significant costs are incurred related to the marketing and legal setup of the fund. There are some cases where these startup expenses are paid on a pro-rata basis by the LPs.

Another source of expense occurs when a fund uses outside advisors to help source, evaluate and advise portfolio companies. These advisors can be paid in a variety of ways, but most often are paid through a share of the GP carry and some cash from the annual management fees.

In addition to receiving compensation from management fees and carry, should VCs expect to receive compensation if they take a board seat on a portfolio company?

Here’s a typical structure for an early stage board:

-

1 or 2 from the Management Team: CEO and a co-founder

-

1 or 2 Investor(s)

-

1 or 2 Independent Director(s)

For the management directors, compensation practice is typically just their ordinary compensation and bonus plan and perhaps participation in the company’s option plan (since they likely already have a lot of founder stock.) For independent directors, it is typical to give options or restricted stock units totaling 0.25%-1.5% of the company. But when it comes to the investor board seats, compensation can vary by type of investor. It is not uncommon for individual angels to be paid modest compensation in the form of stock. However, the VC investor component of the board is a bit different for a few reasons:

-

First, they appointed themselves by contractual right

-

Second, they are already major shareholders by way of their fund, and

-

Third, in the case of VCs, they are already being paid a management fee, and some carry for duties like board service. It’s their day job.

For these reasons, it’s unlikely that a VC will get additional stock in a company through board compensation. Furthermore, in some fund agreements, any compensation received through board director fees may ultimately reduce the annual management fee paid to the fund. Bottom line… don’t expect to boost your income through board compensation.

So with all we discussed above, what level of compensation can a VC make running an early stage venture fund?

There are numerous factors that drive overall compensation for a VC in a venture fund. Let’s take a quick look at each of these factors and then we can run a few example cases to see what range of compensation a VC can expect from an early stage fund.

-

Fund Size: Are you running a $10M, $50M or $100M fund?

-

Management Fee: Is your fee typical at 2% or are there other factors such as a lower fee for an anchor LP?

-

Carry: Is your carry typical at 20%?

-

Fund Returns: Was your fund a top performing fund returning 3X committed capital or did you underperform and end up close to 1.5X?

-

Number of GPs: Is the firm run by 2 GPs who split the carry evenly or do you have more GPs along with venture partners and advisors who receive some of the carry?

These five factors are the single biggest contributors to overall compensation for a VC. For small funds managing under $20M, the operating expenses of the fund (e.g. rent, employees, advisor fees, etc.) can eat up a substantial portion of the annual management fee. In that situation, the majority of the VC’s compensation comes from the carry driven by strong fund performance.

In the table below, we will run through a few examples that are based on the five key factors listed above. In order to simplify the exercise, we will make some assumptions, including:

-

Half the management fee goes to overhead and half is paid out to the GPs

-

The management fee is set at 7.5% of committed capital over the 10 years life of the fund

-

The fund is run by 3 GPs who split the carry and remaining management fee evenly

-

Carry is set at 20%

-

The LPs contribute 100% of the fund’s capital - no capital comes from the GPs

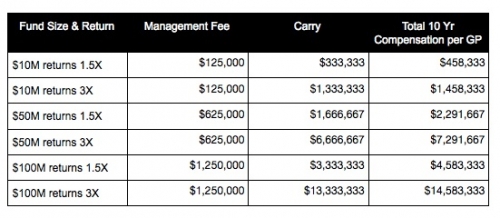

Finally, we will look at three fund sizes: $10M, $50M and $100M, and those funds will either return 1.5X or 3X. Please note: the payouts listed in the table are based on the compensation paid per GP over the full 10 years of the fund.

Let’s take a closer look at these numbers. In the first scenario where a $10M fund returns 1.5X of capital, each GP will earn $125,000 in management fees over the 10 year fund life and will be paid an additional $333,333 in carry. Over the full 10 years of the fund, each GP makes approximately $450K, or $45K per year and that is an average - in the early years they will make nothing. In the scenario where this $10M fund returns 3X of invested capital, the GPs make approximately $145K per year. Doesn’t look like you are going to get rich managing a $10M fund.

Now let’s look at the best case scenario from this table. A $100M fund that returns 3X of invested capital will pay out $14.5M to each of the GPs over the 10 year life of the fund. Now it’s starting to get interesting! Average annual compensation exceeds $1M, but remember, most of that compensation will come in the latter years of the fund as companies exit and carry gets distributed.

To help you dig into venture fund compensation and allow you to play around with key assumptions, we’ve built a modeling tool that you can adjust and build scenarios with. We designed this tool to allow you to factor in the five major assumptions on venture compensation along with some of the other factors that will drive your results.

As you contemplate some of the foregoing material, I am sure you are realizing that the VC fund business is not all that different from other areas in life. Performance tends to get rewarded, and there are no real shortcuts or ways to get rich quick. This is not intended to be discouragement. Fund work is some of the most interesting work a person can do, and may have tremendous ancillary benefits with impact funds or affiliated funds. And, if it turns out that you are good at it and have a little luck, you might find that the leverage inherent in the structures of this industry end up compensating you very handsomely indeed. So by all means, if you think it might be fit for you, give it your best shot!

Want to learn more about managing a fund? Download this free eBook today Venture Capital: A Practical Guide or purchase a hard copy desk reference at Amazon.com.