Note: This article is the fourth in an ongoing series on venture fund formation and management. To learn more about managing a fund, download this free eBook today Venture Capital: A Practical Guide or purchase a hard copy desk reference at Amazon.com.

Staying on top of the early stage investing world requires a lot of reading. In the course of a single day, Christopher and I scan dozens of articles, newsletters, blog posts, and the occasional book chapter or industry podcast. We also read three or four newsletters which focus on activities within the venture community. One of the biggest trends we witnessed over the past few years is the rapid pace of new early stage venture fund formation combined with significant growth in the amount of capital invested.

Staying on top of the early stage investing world requires a lot of reading. In the course of a single day, Christopher and I scan dozens of articles, newsletters, blog posts, and the occasional book chapter or industry podcast. We also read three or four newsletters which focus on activities within the venture community. One of the biggest trends we witnessed over the past few years is the rapid pace of new early stage venture fund formation combined with significant growth in the amount of capital invested.

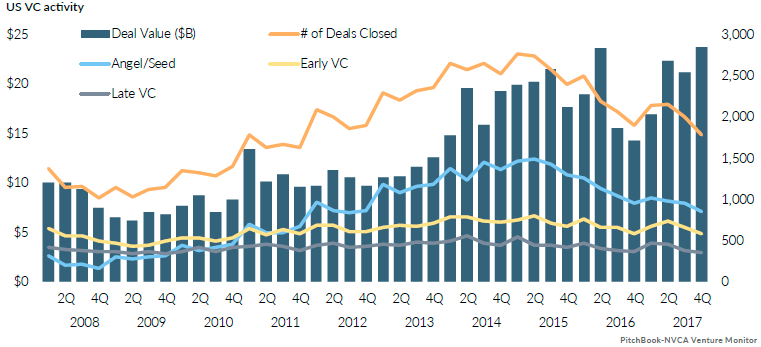

A decade or two ago, most of the new funds were traditional VC funds located in technology hubs in the US and a few other countries around the globe. These days, funds are popping up almost everywhere. Growth in venture investing has more than doubled in the US over the past decade as shown in the chart below. If you add statistics from the rest of the world to this data, the growth is even more dramatic.

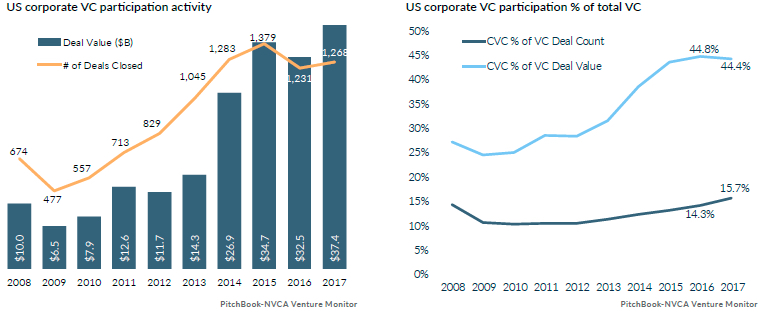

In addition to traditional VC funds, there is significant growth from new types of investors focused on Corporate, Government, University and Social Impact goals. Corporate investors, in particular, are having a major impact on the investment community. As you can see in the charts below, in just under 10 years, US Corporate Venture has gone from ~25% of total venture investment dollars to ~44% of the total dollars.

-

Some attribute this to a trend to reduce capital risk by “outsourcing” research and development to startups who are financed by third parties and then investing in or acquiring the ones showing promise.

-

Others attribute this to a desire to allow more innovation to flourish indirectly despite the more mature conservative corporate culture by owning minority investments in nimble start ups.

-

And still others attribute it to a desire to have an inside track on acquiring attractive start-ups before they raise a ton of venture capital and have their required acquisition price go through the roof.

Regardless of why it is happening, it is clearly an important trend in our current market.

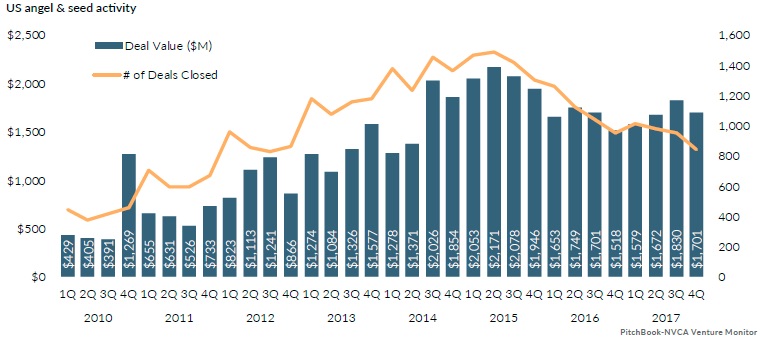

In addition, angel investing is reaching new heights in terms of deals and investment dollars. Angel investments are coming from multiple sources, including groups of angels working together in networks both formal and informal, networks of angels coming together into syndicates, angel funds, family offices, and syndication platforms (such as AngelList, etc.). Just in the past 8 years, total US-based angel investments per year have grown close to 4X. And the numbers shown in the chart below represent just the data that Pitchbook was able to gather. We have seen data from other sources that support activity levels more than twice that shown in this chart.

So what does all this mean? Why should you care? Well, if you are interested in raising a new fund, there appears to be a lot of capital available to invest into early stage companies. And as even better news, this is a very difficult and time-intensive asset class. Most sources of significant capital don’t have the time or the inclination to be an active investor in this sector. Direct investment in smaller deals in early companies are so much work compared to other kinds of investment opportunities available to them. And the failure rate is high, so diversification into a relatively large number of deals is essential. However, for reasons of asset allocation and the desire to chase higher returns, those with significant assets to invest are highly motivated to find a way to participate in the tremendous upside potential offered by this asset class. So committing their money to an early stage venture fund actively managed by experts becomes an attractive option to them (at least in theory).

But how do you go about convincing these prospective investors to trust you with their hard earned capital? Christopher is both a Limited Partner in several venture funds and a General Partner in a couple of seed funds. He has sat on both sides of the fund raising table. He understands what it’s like to be asked to invest in a fund and knows what questions he likes to ask the fund manager. And, he understands what it takes to raise capital from outside investors for the funds he manages. Let’s hear what advice he has to offer to a first time fund manager looking to raise a new venture fund.

Christopher, before we dig into issues around fundraising, can you explain the roles played by a venture fund’s General Partners (GPs) and the fund’s Limited Partners (LPs)?

The General Partners (GPs) of a fund are a team of experienced investors and/or operators who actively run the day-to-day management of the fund, invest its capital, and manage the portfolio. A General Partner (GP) may serve on the board of one or several portfolio companies ensuring the fund’s stake in the investment is looked after.

A Limited Partner (LP) is a qualified investor who commits a certain amount of capital to a fund and pays a management fee (or carry) to the GP to manage his/her investment. LPs may be experienced investors themselves or entirely new to investing. Depending on the fund arrangement, some LPs may be passive investors who solely provide capital, while other LPs may actively participate in a fund by sourcing deals, serving as an industry expert, conducting due diligence, or providing connections or other resources that could help with analyzing the opportunity, enabling growth or identifying exit opportunities.

The terms “limited partner” and “general partner” date back to the early years of venture capital before limited liability companies (LLCs) existed when nearly all the funds in the nascent industry were structured as somewhat complex partnerships with LPs and GPs entering into a partnership agreement spelling out how work would be divided, fees would be assessed and profits would be distributed.

These agreements were complex and carefully designed to minimize legal liability and maximize tax efficiency. Today’s funds are very similar in concept, but can be structured quite differently using limited liability companies (LLCs) and limited liability partnerships (LLPs). Or, a modern fund can even be structured as a combination of LLCs and a traditional partnership agreement whereby the GP is an LLC entity rather than a person or group of people. The fee and profit sharing arrangements in modern funds can be far more complex. As the industry has matured, GPs and LPs have both become more clever, but the goals and the roles remain the same: active investors manage money on behalf of passive partners while minimizing liability and maximizing tax efficiency.

Tell us about your decision-making process before you invest in funds as a limited partner. What were some of the key questions you ask the fund managers?

Let me answer that two ways because I am a somewhat special case. First I will cover the general issues I look at, and recommend any LP review before investing. And then I will show how I applied them in my special situation.

When an LP looks at a fund they should consider three different categories of questions to assess:

-

Team Capabilities

-

Fund Design

-

Fund Status and Current Investing Climate

Team Capabilities

This is really a question of looking at the GPs and figuring out whether they are a team you believe can deliver the superior performance you expect. So you are going to be looking at their general experience base in industry prior to becoming a fund manager, as well as their level of experience and past performance as a GP.

-

What kinds of performance have they delivered for past LPs?

-

How consistent has that performance been over time?

-

What specific companies did they invest in?

-

Are they reporting performance based entirely on one single blockbuster, or have they shown an ability to identify and nurture multiple solid winners?

-

What was their personal role in those investments (lead or just a bystander)?

In addition, you will want to investigate the following:

-

What other professional and personal commitments do they have on their plate that might compete for their time and attention? For example, while lots of board experience is great, if they are already overloaded with board obligations, can they take on new board seats in this new portfolio?

-

How connected and networked are they? How visible are they? Do they have access to the best founding teams (i.e. good deal flow)?

-

How good is their reputation in the community? What kinds of references can they provide from other LPs, founders, VCs?

-

How diverse is the GP team? Do they bring different perspectives and complementary skills to the table?

In short, you are looking for a team with a track record, the skills and the time to invest this new fund successfully. It is a hard job that involves a lot of judgement and intuition. Do these GPs have the chops?

Fund Design

The concept of fund design really encompasses everything from the fund structure to the fund philosophy.

-

What is the fee structure and carry (profit sharing percentage) and how does that compare to market norms?

-

What is the size of the fund?

-

What percentage of the fund is being personally invested by the GPs so they have some skin in the game alongside LPs?

-

How many companies and how much diversification is the fund aiming for?

-

What is the fund's strategy for initial investment vs. total investment over time (and target percentage ownership of each company)?

-

Will the GPs make all the investments directly, or do they plan to employ “scouts” or other agents to represent them in some deals?

Furthermore, you will look to answer the following:

-

In what stage of company will the fund invest (pre-seed, seed, angel, angel extension, pre-Series A, Series A, Series A extension, Series B, or later growth stages)?

-

What is the fund’s overall investment thesis - does it intend to target a particular industry, sector, technology, market space, or other “theme”?

-

What are the criteria the GPs plan to use when evaluating companies?

-

Are there deal structures or deal terms that they will seek out or terms which they will not accept?

-

What is the GPs’ plan for reporting to LPs: minimum statutory requirements (final 2023 rule, fact sheet ), or something more involved?

-

What performance benchmarks do the GPs consider relevant for the fund and what is the team’s expectation in terms of overall performance they will be able to deliver?

By asking these questions, you are going to get an overall sense of what this fund is trying to do that is different from other funds and how and why they believe their unique approach will lead to superior returns.

Fund Status and Fund Climate

Your final set of questions should be about establishing the broader context in which this fund raising is occurring.

-

Is this the GPs’ first (or tenth) fund?

-

How many prior funds are still actively investing (and requiring a lot of time) and how many are in harvest mode?

-

What is the GPs’ current commitment level to those older funds?

-

How long has this particular fund been raising money?

-

How much of this fund has actually been raised so far?

-

When does the fund expect to have a first close and start investing?

-

Are there company investments already earmarked to be added to the fund at inception?

-

Are there special terms being offered to early “anchor” LPs who are willing to come into the first close and get the fundraising ball rolling?

-

What is the fundraising climate right now and are these competitive terms given the current environment?

-

Who are the other LPs committed to the fund and are any of them imposing special LP investment deal terms that are different from those you are offering me, or are any of them imposing special restrictions or constraints on the fund?

As you can see, this is a huge list of questions you need to have a handle on to understand what you are getting into as an LP, and to be able to answer if you are going to raise money as a GP. For a first time GP or LP it can be pretty daunting, but with a little experience and some familiarity with some of the short-hand, it is really not too long a list.

In Part II of this article we'll take a closer at what elements you need to have in a pitch deck or fund prospectus to convince prospective LPs to invest in your fund and what qualifications are important to prospective investors.

Want to learn more about managing a fund? Download this free eBook today Venture Capital: A Practical Guide or purchase a hard copy desk reference at Amazon.com.